Day 948 — Waiting for Seven

Lab Notes: A business I want to own, the price I won’t pay, and the discipline of doing nothing.

There’s a company on the NZX, the New Zealand Stock Exchange, I’ve spent more hours with than I’d care to admit. I’ve read the annual reports. I’ve built the model. I’ve stress-tested the moat, second-guessed the management, and run the demographics out past 2040. I want to own it.

I’m not buying it.

Not today, and probably not this month. Possibly not this year. The business isn’t the problem — I think it’s genuinely wonderful, and I’ll show you why. The problem is the price, and the uncomfortable truth that a wonderful business at the wrong price is just a slow way to lose money you didn’t have to lose.

This is the part of investing nobody puts in the highlight reel. The watchlist that does nothing. The position you’ve researched to death and still don’t hold. Every day the thing trades, and every day I do nothing, and the doing nothing is the entire discipline. It feels like inaction. It’s actually the hardest decision I make all week, repeated until something changes.

So this is a lab note about waiting — what I’m waiting for, the number I’m waiting for, and whether I’m being disciplined or just stubborn. By the end, I’ll have put a price on the record. You’ll get to watch whether I hold the line.

The business

The business is Summerset Group (NZX: SUM, ASX: SNZ), a retirement-village operator with around 40 villages across New Zealand and a growing Australian footprint. The model is one of the most elegant structures in commercial real estate, and I’ve yet to find a better local example of capital recycling done well. Build a unit. Sell it on an occupation right agreement for a sum that more than covers the build cost. Keep a deferred management fee of 25% of the original price, accruing over the resident’s stay. When the unit turns over, the resident (or their estate) gets back their money, less the DMF, and the village resells the unit, keeping all of the capital appreciation. The original capital has now built and sold the same unit twice, while the weekly fees have paid the operating costs in between.

Lay that loop on top of an aging population — New Zealand’s over-75 cohort is forecast to roughly double in twenty years — and you have a structural growth machine that doesn’t need to leverage itself into oblivion to compound.

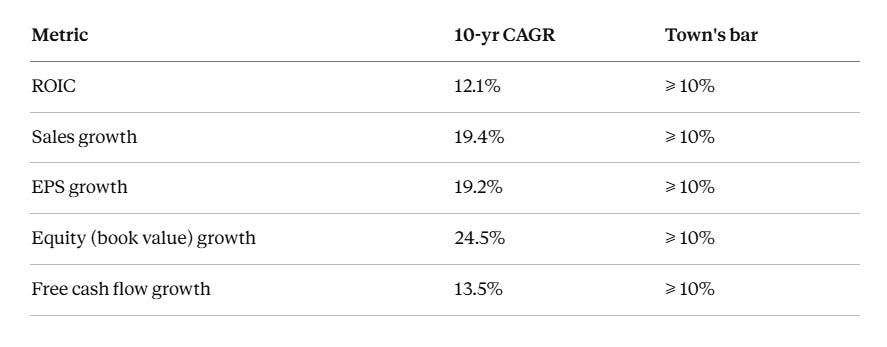

So what does it look like by the numbers? Phil Town’s Rule #1 framework demands a business clear five hurdles over a ten-year window — return on invested capital, sales, earnings, equity (book value), and free cash flow growth, all comfortably above 10% per year. The bar is deliberately high. Most listed companies fail at least one. Here’s Summerset’s scorecard:

Five for five. Not one limps. The business has roughly doubled its book value every three years, grown the top line and per-share earnings at nearly 20% a year for a decade, and done it while earning a genuine 12% on every dollar of capital put to work. This is exactly the profile Town tells you to hunt for — the rare company that compounds on every axis at once.

So the only question worth this article is the one the framework cares about most: at what price?