Day 962 — Punching the Card

Lab Notes: A Sin Stock, a Fat Pitch, and the Filter That Required Real Work

"The big money is not in the buying and the selling, but in the waiting." — Charlie Munger

Last week, I wrote about Buffett’s 20-slot punchcard concept and the two recent investments I should have made and didn’t. The piece ended on a line I meant: the card is there to be punched.

This edition is what that looks like in practice. A position I did take, in mid-March, just before this newsletter began. Around 5% of net wealth. A meaningful commitment, made with the framework from the previous piece doing exactly what frameworks are supposed to do: making the decision easier when the moment arrives.

A note before I begin: I hold this position as I publish. If the thesis breaks, you’ll get the update. That’s the deal when I write about live positions, and I’d rather commit to it upfront than pretend otherwise.

The Screen That Started It

I run a screener built on Phil Town’s Rule #1 criteria — the Big Five growth rates plus return on invested capital, scored together. Most weeks, nothing interesting comes out of it. The market is reasonably efficient most of the time, and businesses that compound at high rates usually trade at multiples that price that compounding in.

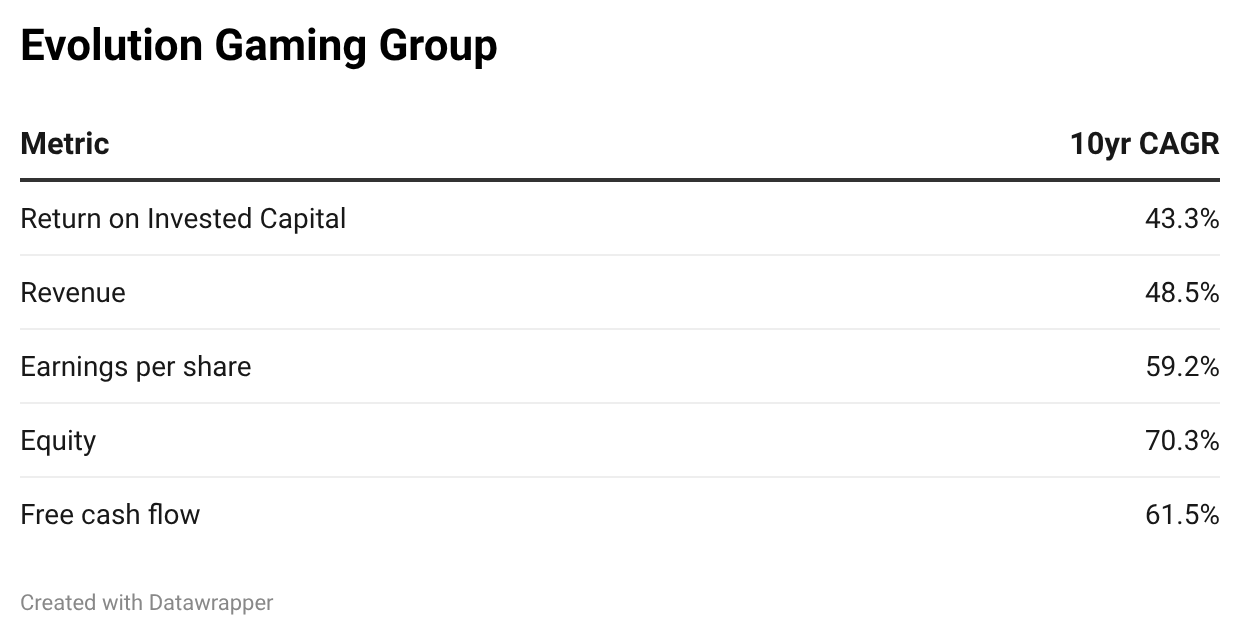

Then occasionally, the screen returns something that doesn’t make sense at first glance. One name sat at the top of the list with a P/E around 11, a ROIC above 40%, and earnings compounding at roughly 60% a year. Rule #1 asks for 10% on those growth rates as a minimum filter. This company was clearing the bar by four to six times. ROIC above 40% on a P/E of 11 is the kind of dislocation that, in an efficient market, isn’t supposed to sit on a public screener at all.

The company is Evolution Gaming Group (LSE: 0RQ6, ADR: EVVTY). The first reaction to numbers like that is the right one: something must be wrong. The screen is showing you a business that the market has decided not to value, and the market is not usually that stupid. Your job is to figure out what the market knows that you don’t, and then decide whether they’re right.

So I worked the Four Ms — Meaning, Moat, Management, Margin of Safety — from last fortnight’s piece. What follows is the walk-through, including the one filter where I had to think hardest, and how I got from the screen result to a meaningful position in mid-March.

For free readers: the short version is that I concluded the dislocation was real, took the position, and expect to hold it for years. The paid section below is the actual work — why the moat is structural, how I got comfortable with the management question that has the market spooked, and why a P/E of 11 looks to me like a 50% margin of safety rather than a value trap.