Day 983 - The Boring Path to Extraordinary Returns

Filed Under: Investing Lab Notes

Let me be upfront about something: I am not the person you’d expect to be writing about financial independence.

I still work for income. I hold equities I’ve researched obsessively, then trade erratically. I have, on more than one occasion, identified a genuinely excellent investment opportunity, constructed a reasoned thesis, watched the price move exactly as expected, and done nothing.

So take this less as a masterclass and more as a field report from someone who has learned certain lessons more painfully than necessary.

What makes a great business

Warren Buffett’s core thesis, stripped to its bones: buy excellent businesses at reasonable prices, and hold them. The wealth accumulates.

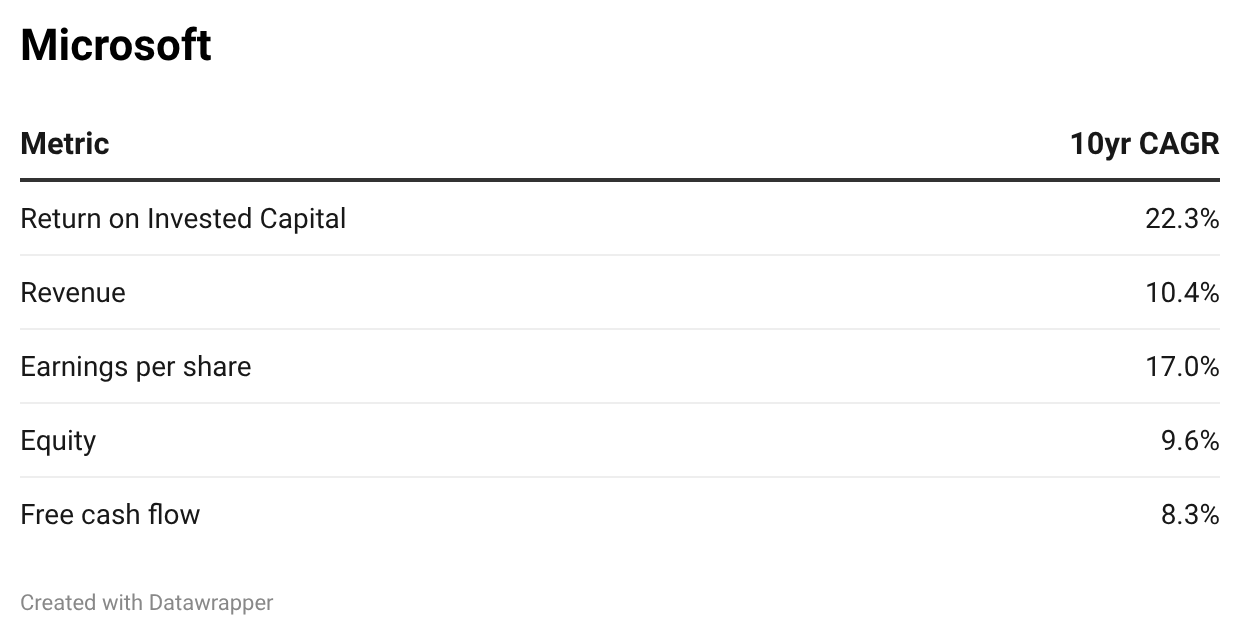

The question is: what does “excellent” look like in numbers? I’ll write a proper breakdown of the full Buffett-style checklist another time, but here’s the short version: you want a business that earns outsized returns on the capital it deploys, and grows — in revenue, earnings, equity, and free cash flow — consistently over a long period. Not one good year. A decade.

As a benchmark, here are Microsoft’s 10-year compounded annual growth rates:

These are genuinely strong numbers. Microsoft is one of the most valuable businesses in the world. This is what a great company looks like.

These are the numbers of one of the most successful businesses of the last decade. The company I spotted had numbers that made these look pedestrian. More below.